The Best Guide To Mortgage Investment Corporation

The Best Guide To Mortgage Investment Corporation

Blog Article

The Greatest Guide To Mortgage Investment Corporation

Table of ContentsHow Mortgage Investment Corporation can Save You Time, Stress, and Money.Unknown Facts About Mortgage Investment CorporationAbout Mortgage Investment Corporation7 Easy Facts About Mortgage Investment Corporation ExplainedMortgage Investment Corporation Things To Know Before You Get This

Does the MICs credit rating board evaluation each mortgage? In many situations, home loan brokers manage MICs. The broker must not act as a member of the credit score committee, as this places him/her in a straight conflict of rate of interest given that brokers normally gain a commission for putting the home mortgages.Is the MIC levered? The financial organization will accept specific home mortgages owned by the MIC as safety and security for a line of debt.

It is important that an accounting professional conversant with MICs prepare these statements. Thank you Mr. Shewan & Mr.

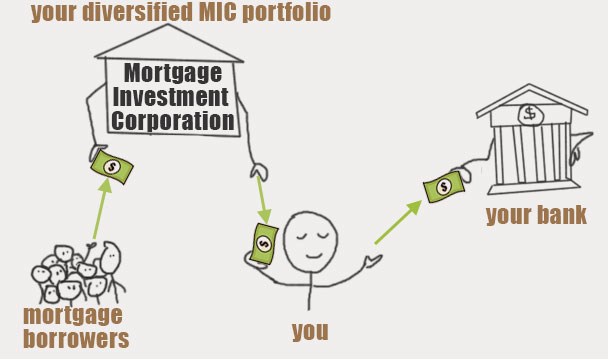

Last updated: Upgraded 14, 2018 Few investments are as advantageous as useful Mortgage Investment Home mortgage Financial InvestmentCompany), when it comes to returns and tax benefitsTax obligation Since of their corporate framework, MICs do not pay income tax obligation and are legally mandated to disperse all of their incomes to capitalists.

This does not imply there are not threats, but, usually speaking, whatever the broader stock exchange is doing, the Canadian realty market, particularly significant cities like Toronto, Vancouver, and Montreal does well. A MIC is a firm formed under the policies establish out in the Income Tax Obligation Act, Area 130.1.

The MIC earns earnings from those home mortgages on interest charges and general charges. The actual appeal of a Home loan Financial Investment Firm is the yield it offers financiers contrasted to other fixed earnings financial investments. You will certainly have no trouble finding a GIC that pays 2% for an one-year term, as federal government bonds are similarly as reduced.

Fascination About Mortgage Investment Corporation

A MIC needs to be a Canadian corporation and it have to spend its funds in mortgages. That claimed, there are times when the MIC ends up owning the mortgaged property due to repossession, sale agreement, and so on.

A MIC will gain rate of interest income from home loans and any cash the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to shareholders, the MIC does not pay any kind of income tax obligation. Rather than the MIC paying tax on the interest it makes, shareholders are accountable for any type of tax obligation.

About Mortgage Investment Corporation

And Deferred Strategies do not pay any tax obligation on the rate of interest they are approximated to get - Mortgage Investment Corporation. That claimed, those who hold TFSAs and annuitants of RRSPs or RRIFs might be hit with particular penalty tax obligations if the investment in the MIC is thought about to be a "prohibited financial investment" according to copyright's tax code

They will guarantee you have discovered a Home mortgage Investment Firm with "competent financial investment" status. If the MIC qualifies, it can be very helpful come tax time considering that the MIC does not pay tax obligation on the interest earnings and neither does the Deferred Strategy. More extensively, if the MIC falls short to meet the demands established out by the Revenue Tax Act, the MICs earnings will certainly be strained before it gets distributed to shareholders, decreasing returns significantly.

It appears both the genuine estate and supply markets in copyright are at all time highs Meanwhile yields on bonds and GICs are still near document lows. Also cash is losing its charm due to the fact that energy and food prices have pressed the rising cost of living price to a multi-year high.

The Best Strategy To Use For Mortgage Investment Corporation

Numerous hard working Canadians that desire to get a home can not obtain home loans from standard his response banks because perhaps they're self employed, or do not have a well-known debt background. Or perhaps they want a brief term loan to create a big residential property or make some improvements. Financial institutions have a tendency to ignore these possible debtors since self employed Canadians do not have steady incomes.

Report this page